Business Credit Cards With No Personal Guarantee: The Real 2026 List

Almost every traditional business credit card from Amex, Chase, Capital One, and Citi requires a personal guarantee — meaning if the business defaults, the issuer can come after your personal credit and personal assets. A true business credit card with no personal guarantee underwrites the entity, not you. In 2026 there are six mainstream options that genuinely qualify, plus a handful that get incorrectly listed as no-PG. This guide separates the real list from the marketing claims, with eligibility, limits, and which card fits which stage of business.

HubNo Personal Guarantee Cards →By Sarah Chen · Lead Media Buyer & Credit Card Strategist

Published May 28, 2026 · 11 min read · How we review

What 'no personal guarantee' actually means

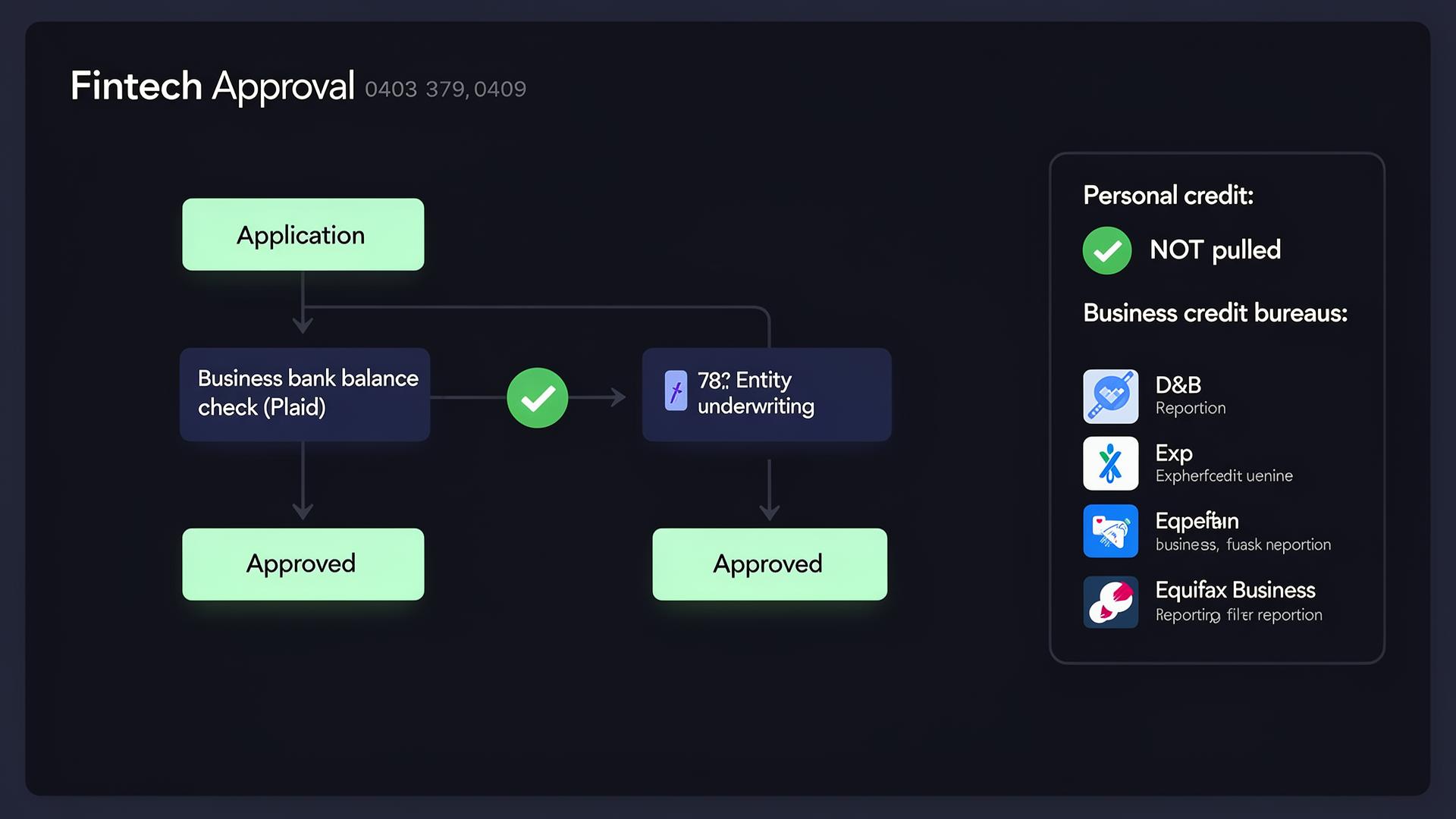

A personal guarantee is a clause that makes you, the owner, personally liable for the card's debt if the business cannot pay. With a true no-PG card the issuer underwrites the entity's bank balance, revenue, and cash flow — not your FICO. Default risk stays at the business level. Three practical consequences: (1) the issuer typically pulls no personal credit on application, so opening the card doesn't hurt your personal report, (2) balances and utilization never appear on your personal credit file, (3) a business default cannot be pursued against your personal assets. The trade-off: no-PG cards require established business banking, real revenue, or venture funding — they're not available to a brand-new sole proprietorship.

Brex — the original no-PG corporate card

Brex underwrites on business bank balance and revenue. Eligibility: incorporated entity (LLC, C-corp, S-corp — no sole props) with $50K+ in a business bank account or $100K+ in monthly processed revenue. Limits scale dynamically with deposits, typically 10–20% of cash balance for the daily-pay plan. Rewards: 7x on rideshare, 4x on Brex Travel, 3x on restaurants, 2x on software, 1x on everything else — including ad spend. No annual fee. Best for: VC-backed startups and agencies with strong cash reserves that need high limits and clean spend controls more than they need ad-spend rewards.

Ramp — no-PG, no fees, 1.5% flat cashback

Ramp underwrites similarly to Brex but is more flexible on revenue requirements. Eligibility: incorporated entity with at least $25K in a verified business bank account. Limits scale with cash and average 10–15% of bank balance. Rewards: a flat 1.5% cashback on everything, including Meta and Google ad spend, paid as statement credits. No annual fee, no FX fees, no late fees. Best for: small-to-mid-size agencies that want zero personal-credit exposure and excellent expense automation, and accept the rewards gap versus Amex/Chase as the cost of a no-PG setup.

Rho — no-PG card with treasury and AP built in

Rho is the dark-horse pick. Underwrites on cash balance (typically $100K+) and revenue. No PG, no personal credit pull, no fees on the card itself. Rewards: 1.25% cashback on all spend with no category restrictions. Best for: profitable agencies and SMBs that want their corporate card, treasury, AP, and FX all in one platform without giving the card issuer a hook into personal credit. Limits are conservative early but expand with deposits and clean payment history.

Mercury IO Card (and Mercury Credit) — no-PG for Mercury banking customers

Mercury offers an IO Mastercard (charge card, pays in full daily or monthly) and Mercury Credit (revolving). Both require a Mercury business banking account and underwrite on Mercury deposit history. No personal guarantee, no personal credit pull, no annual fee. Rewards: 1.5% cashback on every purchase. Best for: tech startups and remote-first businesses already banking with Mercury that want a single dashboard for cash and corporate card.

Stripe Corporate Card — for Stripe-processing businesses

Stripe's corporate card is no-PG and underwrites on Stripe processing volume. Eligibility: a US-incorporated business processing payments through Stripe. Rewards: 1.5% cashback on top category each month, 1% on everything else. No annual fee. Best for: SaaS companies, e-commerce stores, and marketplaces already running revenue through Stripe — the underwriting is automatic from your processing data, and approval can be instant.

Arc — for venture-backed startups

Arc's corporate card targets venture-backed startups with $250K+ in deposits. No PG, no personal credit pull. Limits are generous against bank balance and runway. Rewards: 1% cashback. Worth knowing about if you're a funded startup, but most agencies will get better economics from Ramp or Brex.

Cards that get incorrectly listed as no-PG (don't fall for it)

Three common false positives. (1) Capital One Spark Cash / Spark Miles for Business — Capital One markets these aggressively to small businesses, but the standard application requires a PG and pulls personal credit. There is a corporate variant for very large accounts, but it's not the public Spark product. (2) Bank of America Business Advantage cards — require PG. (3) Chase Ink series — all require PG. Any traditional bank-issued business card from Amex, Chase, Capital One, Citi, Bank of America, US Bank, or Wells Fargo requires a personal guarantee on the public application, with very rare corporate-tier exceptions for businesses with $10M+ in revenue.

When a personal guarantee is actually fine

If your business is profitable, has reserves equal to 2–3 months of card spend, and your personal finances are stable, a PG is mostly theoretical risk. Amex and Chase business cards rarely report balance and utilization to personal credit if paid on time — only delinquency or charge-off triggers personal reporting. Don't pay 4–6 percentage points in foregone rewards (Amex Gold's 4x category vs Ramp's 1.5x flat) to avoid a low-probability risk — see the full cashback vs points math on ad spend before committing. The right play for most agencies is a hybrid: traditional Amex/Chase cards earning maximum rewards on the first $300K of annual ad spend (the best business cards for advertising in 2026), plus a no-PG Ramp or Brex card for overflow, team spend, and limit headroom.

Brex vs Ramp for a business credit card with no personal guarantee

The two most common questions we get: 'Brex or Ramp?' and 'which business credit card with no personal guarantee should I apply to first?'. Short answer: apply to Ramp first if you're under $100K in business banking, apply to Brex first if you're VC-backed or sitting on $250K+. Long answer: Ramp's underwriting is more forgiving on revenue volatility, the dashboard is cleaner for non-finance founders, and the 1.5% flat cashback on ad spend beats Brex's 1x on ads (deeper dive in our Ramp Card review for media buyers). Brex wins on travel rewards (7x rideshare, 4x on Brex Travel), on raw limit size for funded startups, and on integrations with NetSuite / QuickBooks for finance teams. For the full head-to-head including Amex, see Brex vs Ramp vs Amex for ad spend. Both are genuine business credit cards with no personal guarantee, both pull zero personal credit, both report only to the business — the choice is operational fit, not credit quality.

Easiest business credit card to get with no personal guarantee

If 'easiest' means lowest eligibility bar in 2026, Ramp wins — $25K in a verified business bank account is the only hard floor. If 'easiest' means fastest approval, Stripe Corporate Card wins for businesses already processing on Stripe (approval can be instant from processing data). If 'easiest' means most forgiving on a thin business credit file, Mercury IO Card wins for anyone already banking with Mercury — the deposit history is the underwriting. The hardest of the six is Arc, which targets venture-backed startups with $250K+ in deposits and isn't realistic for a bootstrapped agency. None of these cards require an established business credit file the way a Chase Ink or Amex Business would expect for a personal guarantee underwrite — that's the whole point.

Business credit cards with no personal guarantee for LLCs

All six cards on this list (Brex, Ramp, Rho, Mercury IO, Stripe Corporate, Arc) are explicitly available to single-member and multi-member LLCs, as well as C-corps and S-corps. The only structure they don't underwrite is the sole proprietorship — because legally a sole prop has no separation between owner and business, so there's no entity to underwrite. If you're operating as a sole prop today, the path to a business credit card with no personal guarantee is: form an LLC (~$50–$300 depending on state), get an EIN from the IRS (free, 10 minutes online), open a business bank account in the LLC's name, deposit operating capital, run 30–60 days of revenue through the account, then apply. Total elapsed time is typically 60–90 days from sole prop to approved Ramp or Brex card with no PG.

Do business credit cards with no personal guarantee build business credit?

Yes — and this is one of the underrated benefits of a no-PG card. Brex, Ramp, and Rho report payment history to the major commercial credit bureaus (Dun & Bradstreet, Experian Business, Equifax Business). On-time payments build the business's Paydex and Intelliscore over 6–18 months, which then unlocks larger no-PG limits, trade lines from suppliers, and eventually traditional bank business lines of credit without a personal guarantee. Mercury IO and Stripe Corporate report less consistently — verify directly with the issuer if business-credit building is a priority. None of these cards report to your personal credit bureaus (Equifax, Experian, TransUnion consumer), so utilization and balances stay completely separated from your personal FICO.

How to apply for a business credit card with no personal guarantee in 2026

The application itself takes 10–20 minutes for all six issuers and is entirely online. You'll need: the LLC or corporation's legal name, EIN, formation state, formation date, business address, NAICS code or industry description, estimated annual revenue, and the business bank account credentials (connected via Plaid so the issuer can underwrite the actual balance and transaction history). You'll provide an SSN for identity verification under the Patriot Act, but the credit decision and ongoing reporting are at the business level — your personal credit file is untouched. Approval decisions for Brex, Ramp, and Stripe are typically instant or within 24 hours. Rho and Mercury can take 2–5 business days. Limits start in the $5K–$50K range for early-stage businesses and scale to seven figures monthly for established agencies and funded startups.

Takeaway

Brex, Ramp, Rho, Mercury, Stripe, and Arc are the six business credit cards with no personal guarantee that actually exist in 2026. Use them as the overflow / team-spend layer of your credit stack — keep traditional Amex and Chase business cards for the first $300K of ad spend per year where rewards are 3–4x higher, then layer no-PG for scale, limit headroom, and personal-credit protection.

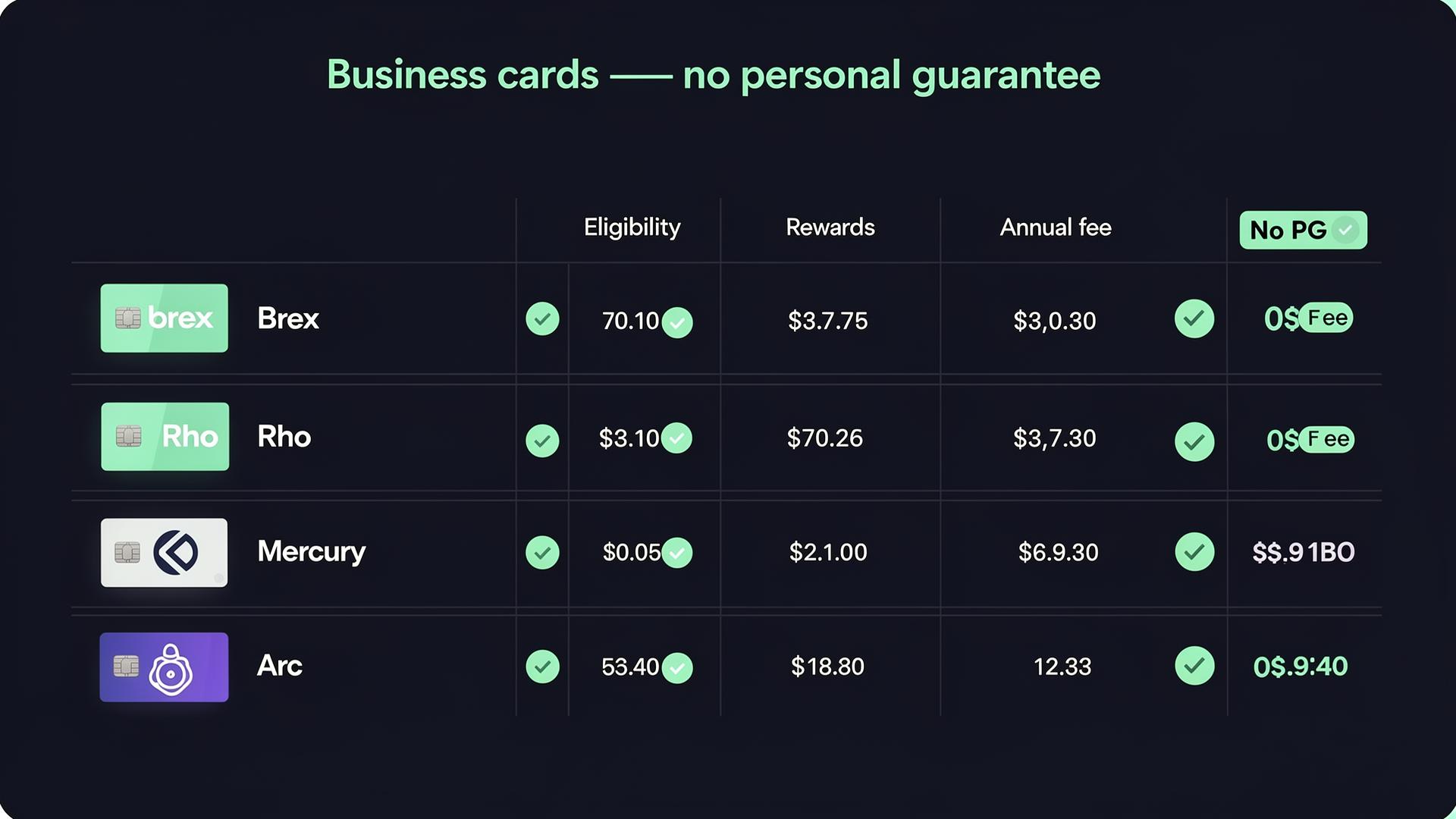

Business credit cards with no personal guarantee — 2026 comparison

All six cards skip the personal guarantee and the personal credit pull. Eligibility is the real differentiator.

| Card | Eligibility | Rewards | Annual fee | Best for |

|---|---|---|---|---|

| Brex | Incorporated entity, $50K+ bank balance or $100K+/mo revenue | 7x rideshare · 4x travel · 3x dining · 1x ads | $0 | VC-backed startups, high-cash agencies |

| Ramp | Incorporated entity, $25K+ in verified business bank | 1.5% flat cashback (incl. ad spend) | $0 | Small-to-mid agencies, expense automation |

| Rho | Incorporated entity, ~$100K+ deposits | 1.25% flat cashback | $0 | Profitable SMBs needing card + treasury + AP |

| Mercury IO Card | Mercury banking customer | 1.5% flat cashback | $0 | Tech startups already on Mercury |

| Stripe Corporate Card | US business processing on Stripe | 1.5% top category, 1% other | $0 | SaaS, e-commerce, marketplaces on Stripe |

| Arc | Venture-backed startup, $250K+ deposits | 1% cashback | $0 | Funded startups with high burn |

How to qualify for a business credit card with no personal guarantee

If you're not yet eligible for Brex, Ramp, or Rho, this is the 6-step playbook to get there in 60–90 days.

- 1

Form a real entity

Register an LLC or C-corp in your state. No-PG issuers cannot underwrite a sole proprietorship because there's no separate legal entity to underwrite. Stripe Atlas, LegalZoom, or your state's online portal will set up an LLC in 1–2 weeks for $50–$500 depending on state.

- 2

Get an EIN from the IRS

Apply for an Employer Identification Number directly at irs.gov — free, takes about 10 minutes online. The EIN is the business's tax ID and the identifier no-PG issuers will underwrite against.

- 3

Open a dedicated business bank account in the entity name

Mercury, Brex Cash, Rho, Relay, or a traditional bank — all work. The key is that the account is in the LLC's legal name, funded from business revenue, and used exclusively for business transactions. Issuers can see this account and use it to underwrite.

- 4

Deposit and maintain at least $25K–$50K of operating capital

Ramp accepts applications at $25K. Brex prefers $50K+ for fastest approval. Build the balance through retained earnings or by capitalizing the LLC from owner funds, and keep it parked there for at least 30 days before applying so the issuer sees stable cash.

- 5

Run 30+ days of real revenue through the account

Issuers underwrite on cash flow as well as balance. Route customer payments, Stripe payouts, or invoice payments through the business account so the underwriting model sees consistent inflows. A pure capitalization deposit without revenue activity often gets lower limits.

- 6

Apply for Brex, Ramp, or Rho — and connect the bank account

Submit the application using the EIN, the LLC's legal name and address, and connect the business bank account via Plaid during the application. Decisions are typically instant or within 24 hours. Start with Ramp if you're under $100K in balance; start with Brex if you're VC-backed or above $250K in cash.

Frequently asked questions

Are there really business credit cards with no personal guarantee?

Yes — Brex, Ramp, Rho, Mercury IO Card, Stripe Corporate Card, and Arc are the six mainstream business credit cards with no personal guarantee in 2026. They underwrite the business entity's bank balance, revenue, or processing volume instead of your personal FICO. Every traditional card from Amex, Chase, Capital One, Citi, and the major banks requires a personal guarantee on the public application.

Will a no personal guarantee business credit card hurt my personal credit?

No. Genuine no-PG cards do not pull your personal credit on application, do not report balance or utilization to personal credit bureaus, and cannot be reported as a default on your personal file because the business is the only legal obligor. The trade-off is that you also don't build personal credit through the account.

Can I get a no-PG business credit card as a sole proprietor?

Generally no. Brex, Ramp, Rho, Mercury, Stripe, and Arc all require an incorporated entity — LLC, C-corp, or S-corp — and a business bank account in the entity's name. Sole proprietorships have no legal separation between owner and business, so issuers have no entity to underwrite. The fastest path is to form an LLC (typically $50–$300 depending on state), open a business bank account, deposit operating capital, then apply.

What's the minimum bank balance for a Brex or Ramp no-PG card?

Ramp accepts applicants with as little as $25K in a verified business bank account. Brex officially requires $50K in business banking or $100K+ in monthly processed revenue, though approvals at lower thresholds happen for venture-backed startups with runway. Both increase limits dynamically as deposits grow.

Do no personal guarantee business cards earn good rewards on Facebook and Google ads?

Honestly, no — not compared to Amex Business Gold (4x category, capped at $150K/year) or Chase Ink Preferred (3x on social/search ads, $150K cap). Ramp, Brex, Mercury, and Stripe all pay 1–1.5% cashback on ad spend. The 4–6 percentage-point rewards gap is the real cost of skipping the personal guarantee. Most agencies run a hybrid stack: Amex/Chase for the first $150K of ad spend at premium rates, no-PG card for everything above.

Is Capital One Spark a no personal guarantee business card?

No. The publicly available Capital One Spark Cash and Spark Miles for Business cards both require a personal guarantee and pull personal credit on application. Capital One has corporate-tier products that skip the PG, but those are reserved for businesses with $10M+ in annual revenue and are not available through the standard online application.

What's the easiest business credit card to get with no personal guarantee?

Ramp has the lowest eligibility floor of any business credit card with no personal guarantee in 2026: a verified business bank account with $25K in deposits. Brex is similarly accessible for VC-backed startups regardless of revenue. Stripe Corporate Card is the fastest to approve for any business already processing payments on Stripe — the underwriting is automatic from your processing volume.

Do business credit cards with no personal guarantee build business credit?

Yes. Brex, Ramp, and Rho report on-time payments to Dun & Bradstreet, Experian Business, and Equifax Business. Over 6–18 months of clean payment history, your business builds a Paydex and Intelliscore strong enough to qualify for higher no-PG limits, supplier trade lines, and eventually traditional business lines of credit without a personal guarantee. None of these cards report to your personal credit bureaus.

Can a startup get a business credit card with no personal guarantee?

Yes — Brex and Arc are specifically designed for venture-backed startups. Brex underwrites on cash balance and runway; Arc requires $250K+ in deposits but offers larger limits. Ramp and Stripe also accept bootstrapped startups with $25K+ in business banking or active Stripe processing volume. The only requirement common to all six issuers is an incorporated entity (LLC or C-corp) — no sole proprietorships.

Will applying for a business credit card with no personal guarantee show on my personal credit report?

No. Brex, Ramp, Rho, Mercury IO, Stripe Corporate, and Arc all underwrite on the business entity and pull zero personal credit on application. The application will not generate a hard inquiry on your Equifax, Experian, or TransUnion consumer file. The only personal data collected is an SSN for Patriot Act identity verification — not a credit pull.

Apply directly to the cards in this guide

Editor-vetted offers. We may earn a referral fee when you're approved — at no cost to you.

Ramp Business Corporation

Ramp

No personal guarantee, no annual fee, 1.5% flat cashback on every dollar — including Meta and Google ad spend. $25K business banking minimum.

Up to $1,500 welcome bonus for new customers

Apply for Ramp →Brex Inc.

Brex

No personal guarantee, no annual fee, dynamic limits that scale to 7 figures monthly. 7x rideshare, 4x Brex Travel, 1x on ads. Best for VC-backed startups and high-cash agencies.

Up to 110,000 Brex Rewards points on qualifying spend

Apply for Brex →Advertiser disclosure: this page contains affiliate links. We only feature cards we've evaluated for ad-spend use cases.

About the author

Sarah started her media-buying career in 2017 at a Shopify Plus agency in Austin, scaling a portfolio of fashion and beauty brands from $200K to $14M in annual revenue through Meta ads alone. In 2020 she joined a performance-marketing shop where she managed a $4.2M/month Facebook ad budget across 12 DTC accounts. She holds the Meta Marketing Partner certification and was an early beta tester for Advantage+ Shopping Campaigns. Sarah currently holds the Amex Business Gold, Chase Ink Preferred, Chase Ink Unlimited, Capital One Venture X Business, and Brex — and she uses every one of them weekly against live ad accounts. She covers Meta-focused card strategy, points valuation, and agency stack design on this site.