Cashback vs Points on Ad Spend: Which Wins?

Cashback feels safe. Points feel like leverage. For high-volume Facebook and Meta media buyers, the right answer isn't obvious — it depends entirely on whether you'll actually redeem points well. Below is the full 2026 math at three different monthly spend levels, with the four cards we'd actually recommend in each lane.

HubMeta Payment Systems →By Marcus Rivera · Award Travel Analyst & Points Valuation Editor

Published May 31, 2026 · 10 min read · How we review

Cashback economics

The best cashback business cards on ad spend pay roughly 2% flat: Capital One Spark Cash Plus, US Bank Triple Cash Visa (3% on advertising up to $5K/month then 1%), and Ramp / Brex at 1.5% — both available as business credit cards with no personal guarantee. At $15K/month Meta spend = $3,600/year cashback at 2%. Simple, predictable, no redemption work required, and posted as a statement credit so it always lands as real dollars. This is the floor: any media buyer who refuses to learn points should land here, not on a 1% or 1.5% card.

Points economics — naive

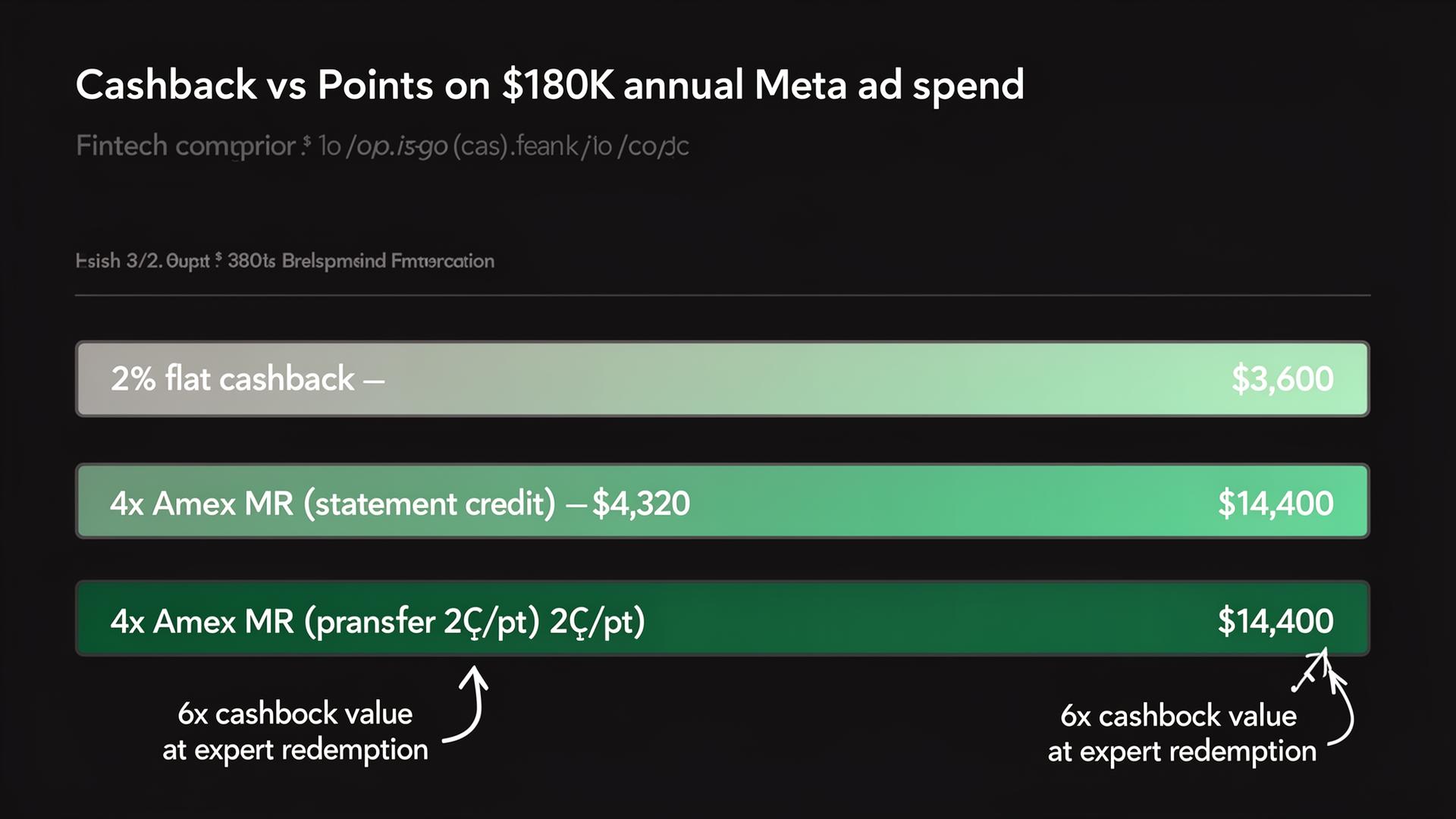

Amex Business Gold at 4x on the same $180K/year of Meta spend = 720,000 Membership Rewards. Redeemed as statement credit at 0.6 cents per point: $4,320/year. Marginally better than the 2% cashback baseline, but you paid $375 in annual fee and learned a new bureaucracy for $345 in incremental return. Not worth the complexity. If statement-credit redemption is your endgame, take cashback.

Points economics — competent

Same 720K MR transferred to airlines and hotels at 2.0 cents per point realized value (Hyatt via Marriott, Air France Flying Blue, Air Canada Aeroplan for North American economy): $14,400/year — 4x the cashback alternative. This is the real reason agencies use Amex Gold or Chase Ink Preferred. The skill level required is one weekend of reading and one transfer per quarter; the payoff is roughly $10K/year per $100K of ad spend.

Points economics — expert

720K MR redeemed at premium-cabin sweet spots (ANA First Class via the Amex transfer partner ANA, Lufthansa First Class via LifeMiles, Hyatt high-category resorts via Marriott Bonvoy transfers) at 3.0+ cents per point: $21,000+/year. 6x the cashback alternative. This requires real award-search skill and date flexibility, but for an agency principal who already takes 2–4 trips a year and pays cash for premium cabin, the math is overwhelming.

Cashback vs points at $5K, $15K and $50K monthly Meta spend

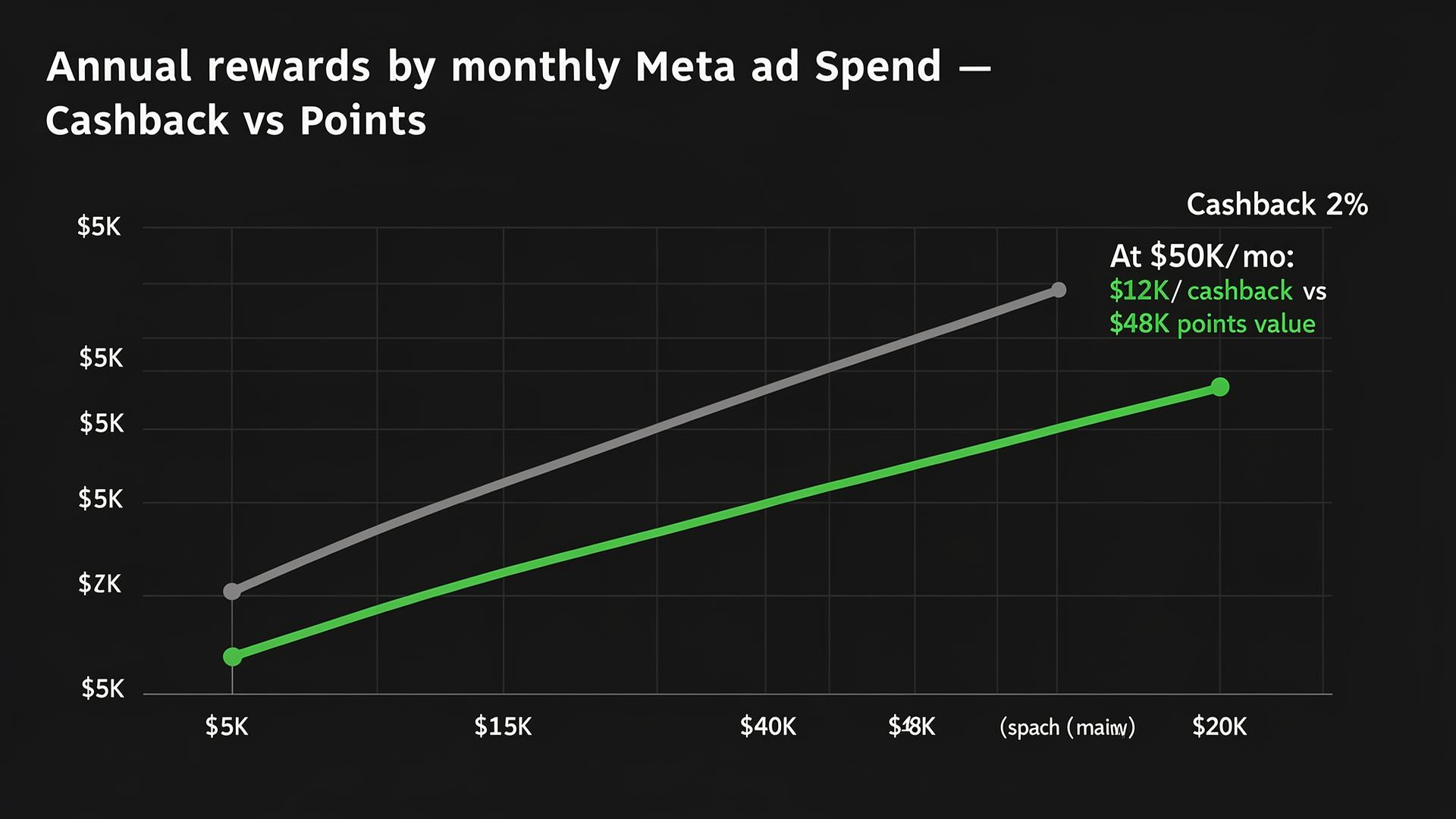

At $5K/month ($60K/year): 2% cashback = $1,200. 4x Amex Gold expert = $7,200. Net edge to points: $6,000/year — but $375 annual fee + redemption work might not be worth it for one principal. At $15K/month ($180K/year): cashback = $3,600, expert points = $21,600. Net edge: $18,000/year. Points clearly win — see best credit card for $10K/month Facebook ad spend for the full setup at this tier. At $50K/month ($600K/year), you hit Amex Gold's $150K cap and need to stack — capping Gold at 4x for the first $150K then layering Chase Ink Preferred 3x for the next $150K then Venture X Business 2x for the rest: ~$48K/year in well-redeemed points vs $12K cashback. Net edge: $36K/year — that's the agency setup we break down in best credit card for $50K+/month media buyers. At this scale only liquidity-constrained agencies should stay on cashback.

Hybrid stacks: cashback for some categories, points for others

The most common 2026 setup at any real media-buying agency: points cards for ad spend (Amex Gold + Chase Ink Preferred — full ranking in the best business credit card for advertising spend in 2026), cashback cards for everything else (Ramp or Brex flat 1.5% on SaaS, contractor payments, lunches, ride-share). Reasoning: ad spend is the largest and most concentrated category — that's where points returns scale. Operating expenses are diffuse and lower-value per transaction — that's where simplicity matters more than redemption ceiling. Don't pick one or the other; use the right card for the right line item.

When cashback genuinely wins

Three real situations where cashback beats points on ad spend. (1) You won't learn redemptions — pretending you'll book Lufthansa First and never doing it leaves $15K/year on the table; honest cashback at $3,600 is better than pretend points at $0. (2) Your business needs the rebate as cash for operations, not as future travel — early-stage agencies running thin should not park $20K of working capital in MR points 'for later.' (3) Devaluation risk — both Amex MR and Chase UR have devalued sweet spots in the past 24 months; if you cycle balances to zero monthly, cashback eliminates that risk.

Honest answer for your situation

If you'll never book international premium-cabin travel or aspirational hotels and you can't see yourself spending a weekend learning transfer partners: take cashback, run Ramp + a 2% card, move on with your life. If you travel for client meetings or take family vacations and would otherwise pay cash for the flight: take transferable points, learn three sweet spots, and capture $10K–$36K/year of incremental value per $100K of ad spend. The difference between cashback and well-redeemed points is roughly $10K/year per $100K of ad spend — the largest single optimization most media buyers leave on the table.

Takeaway

Points win on raw value if you redeem them well — by 3x to 6x cashback at expert redemption levels. Cashback wins on simplicity and survives devaluations. Be honest about whether you'll learn redemptions — pretend points are worse than predictable cashback. Most serious agencies run a hybrid: points cards on ad spend, cashback cards everywhere else.

Cashback vs points: annual rewards on $180K Meta spend

Same dollar amount, same card categories — redemption strategy changes the outcome by ~6x.

| Strategy | Card | Annual rewards | Effective return |

|---|---|---|---|

| 2% flat cashback | Capital One Spark Cash Plus | $3,600 | 2.0% |

| 1.5% flat cashback (no-PG) | Ramp / Brex | $2,700 | 1.5% |

| 4x points → statement credit | Amex Business Gold | $4,320 | 2.4% |

| 4x points → transfer 2¢/pt | Amex Business Gold | $14,400 | 8.0% |

| 4x points → premium-cabin 3¢/pt | Amex Business Gold | $21,600 | 12.0% |

| 3x points → transfer 2.2¢/pt | Chase Ink Preferred | $11,880 | 6.6% |

Frequently asked questions

Is cashback or points better for Facebook ad spend?

Points beat cashback by 2x to 6x in raw value if you redeem them well — at Amex Business Gold's 4x on ad spend, transferring to airline partners at 2¢/point produces ~8% effective rewards versus 2% cashback. But points only win if you actually redeem them at transfer-partner sweet spots; redeemed as statement credit at 0.6¢/point, the same points are only marginally better than cashback and not worth the complexity.

What's the best cashback business card for ad spend in 2026?

Capital One Spark Cash Plus pays 2% flat on all purchases including ad spend, with no foreign transaction fees and no preset spending limit. US Bank Triple Cash Visa pays 3% on advertising up to $5K/month then 1%. For no-PG options, Ramp and Brex pay 1.5% flat. None of them compete with well-redeemed transferable points (Amex MR, Chase UR) on raw return, but they win on simplicity.

How many points do I earn per $1 spent on Facebook ads?

Amex Business Gold: 4x Membership Rewards (capped at $150K/year on top-two categories combined). Chase Ink Business Preferred: 3x Ultimate Rewards (capped at $150K/year on combined categories). Capital One Venture X Business: 2x miles uncapped on every purchase. Amex Business Platinum: 1.5x MR on individual charges of $5K or more. Ramp / Brex: 1x to 1.5% as cashback equivalent.

Are points or cashback better for taxes?

Both credit card cashback and credit card points received in exchange for purchases are treated by the IRS as rebates, not taxable income. There is no tax difference between earning $3,600 cashback or $14,400 worth of redeemed points on the same $180K of business ad spend. Sign-up bonuses earned without spending requirements (rare) are sometimes treated as taxable income; spend-based bonuses are not.

Can I switch from cashback to points later if I change my mind?

Yes — there's no penalty for closing a cashback card and opening a points card or vice versa. The two practical constraints: Chase's 5/24 rule limits you to opening 5 personal credit cards in 24 months (most business cards don't count toward 5/24 but Capital One business cards do), and you don't want to close a card with banked points before transferring them out — points die with the account at Amex and Chase if no other Membership Rewards or Ultimate Rewards card is open.

About the author

Marcus has been writing about credit card rewards since 2014, with bylines at The Points Guy, Doctor of Credit, and AwardWallet. He specializes in transferable points valuation — building the per-point benchmarks that drive every recommendation on this site. He's redeemed over 8.5 million points across Amex Membership Rewards, Chase Ultimate Rewards, Capital One Miles, and Citi ThankYou, including 14 international first-class redemptions on ANA, Singapore, and Air France. On the business side, Marcus has applied for and held 30+ small-business cards over the past decade and tracks issuer rules (Chase 5/24, Amex once-per-lifetime, Capital One velocity) for every recommendation we make.